Side Projects

I love pursuing interesting economic and financial projects. Here are a few that I worked on in my free time.

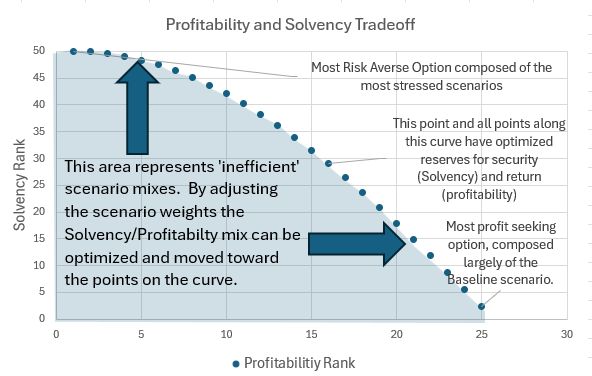

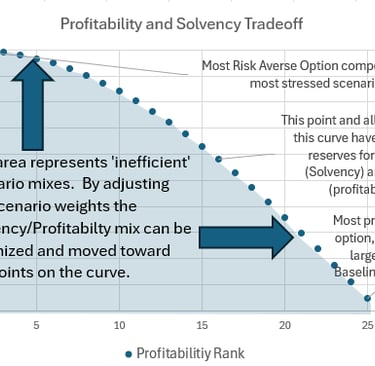

Reserving Efficiency

Built on economic foundations, I took a novel approach to answer the question "What's the most efficient mix of scenarios banks should use when reserving for potential losses?

In an organization using a variety of economic scenarios (downturn, baseline, optimistic) to reserve for losses, this provides the best percentiles of each scenario to match the businesses needs.

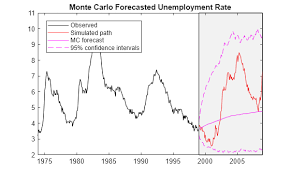

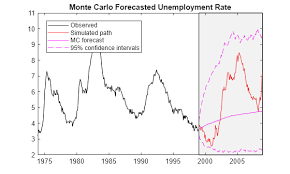

Forecasting the Unemployment Rate Shape

Is economic data sufficiently repeatable where the last 12 months of Unemployment Rate can provide you a better distribution of the next 12 months distribution?

Traditional Monte Carlo uses a Markov Chain assumption, that next periods outcome only depends on this periods outcome. In this project I considered that the path of unemployment matters and that previous periods could impact future period. I sought to match 'shapes' of the previous 12 months relative to the next 12 months.

Project was interesting and provided insight into the failures of many early Large Language Models (LLM). Similar to how if a LLM always forecasts only the most probable next word, you can get an unvaried (problematic) sentence. In my Unemployment Rate forecasting process, my model routinely was caught selecting from a small subset of likely outcomes.

Results: This project was always unlikely to succeed, there's just not enough information in a few historical datapoints to forecast the next year of unemployment. I was enthusiastic about it and enjoyed working through matching algorithms and testing my knowledge of Monte Carlo and Markov Chains.